Finance Committee Gets Briefing on Library Project Finances: Big Questions Remain

Photo: istock

Report on the Meeting of the Amherst Finance Committee, March 3, 2026

This meeting was held over Zoom and was recorded.

Present

Cathy Schoen (Chair, District 1), Lynn Griesemer (District 2), Ana Devlin Gauthier and Sam MacLeod (District 5). Tom Porter (nonvoting member). Absent: Jill Brevik (District 1) and Joseph Jayne (nonvoting member)

Staff: Sean Mangano (Finance Director), Paul Bockelman (Town Manager), and Athena O’Keeffe (Council Clerk)

An update on the financial aspects of the Jones Library building project was on the agenda for the Finance Committee on March 3, 2026. There have been many requests for many months to get details on how the bills are being paid, what kind of borrowing has occurred, how far behind the Library Trustees are in payments to the town, what are the plans to deal with what appears to be a large, looming fundraising shortfall, etc. Some information was shared, but more questions remain unanswered.

Finance Committee Chair Cathy Schoen opened the topic by saying that the agenda item was meant to indicate that the issue of the project financing was planned for the committee’s next meeting on March 17. Town Finance Director Sean Mangano, however, had interpreted the agenda item as a request for him to provide information. There was no written document sent to the committee, but Mangano gave the following information in a verbal report (Managano also provided some additional clarifications after the meeting):

Town Borrowings

The town recently took out a long-term loan of $15,751,810 at 3.85% interest for a 30-year term. The annual debt service on this will be ~$900,000.

The town also recently took out a short-term loan for ~$13.8 million at 2.25% interest with a 1-year term. The interest on this will total ~$286,000. Whatever part of this $13.8 million that is not reimbursed by the Library Trustees will have to be rolled over into long-term borrowing. An additional short-term loan may also be required, depending on when and how much the library pays the town. The town had already taken out a short-term loan for $2.8M last March, which was rolled into this new borrowing. Interest already paid on that was $110,960.

All interest on these loans will be paid by the town. The interest earned on Massachusetts Board of Library Commissioners (MBLC) grant payments received before being spent is kept by the town

MBLC payments

So far, the town has received $8.3 million in payments from the MBLC. Mangano did not know when the next three installments would be received for a grand total of $15.6M.

Library Reimbursement

The Library is obligated to pay the town a total of ~$13.8 million, of which Mangano reported $4.9 million has been received. This does not include the $1 million in Amherst CPA funds for Special Collections that was authorized a few years ago. That leaves $8.9 million for the Jones Capital Campaign to raise and deliver to the town, plus another $1 million it needs to raise to cover its fundraising expenses. This total exceeds the current value of the Jones endowment, which has been identified as the guarantee of repayment to the town but which is also the source of a portion of the library’s annual operating costs.

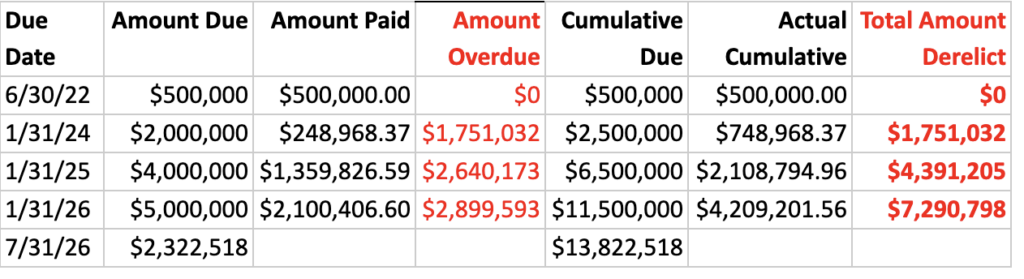

Still No Updated Cash Flow Analysis

The last cash flow analysis for the project was provided in November 2023, when the Library approached the Town Council seeking an additional ~$10 million. The Town Manager promised the Town Council an updated analysis a year ago, when the Town Council reconsidered whether the project should move forward. The following table summarizes the promises made by the library in the original cash flow that was incorporated into the MOU. Also provided are the actual payments made to the town. Not shown is a recent payment of ~$1 million, which brings the total amount that the library is arrears to over $6 million.

Drawdowns on Project Contingency To Be Presented at JLBC on March 9

Mangano said that he would be presenting a financial update on the costs of the project at the next Jones Library Building Committee meeting on Monday, March 9. Contingency funds, which started at $3.6 million, decreased even before construction began, and updates of the amounts spent and still available have not been provided up until now. Contingency dollars will cover the more than $700,000 in change orders to date as well as any increases in soft costs like moving expenses, temporary space costs, furnishings, and OPM, Designer, and other fees.

Further Discussion at Next Finance Committee Meeting

Schoen indicated that this item will remain on the agenda for the March 17, 2026 meeting of the Finance Committee to answer any follow-up questions. She also noted that the Finance Committee has still not received a report from the Community Preservation Act Committee, so it cannot take up their recommendations yet.

The Finance Committee began compiling a list of questions to ask the regional schools, the elementary schools, the town departments, and the library about their operating costs for the upcoming year. These will be discussed at subsequent meetings.

A bank would never lend a large sum of money without knowing the debt to the penny, and without secure knowledge of when and how it will be repaid.

With so many operating and capital budget needs hanging in the balance, I don’t understand why the Town seems in little hurry to ascertain how (or if) the library trustees will come up with their obligation, and when we can expect it. Taxpayers and residents who rely on town services deserve better than the equivalent of “I will gladly pay you Tuesday.”

Might this bankruptcy-law guidance

https://www.nelsonmullins.com/insights/blogs/red-zone/bankruptcy-101/unique-issues-faced-by-non-profits-in-bankruptcy

be useful for understanding the challenging financial relationship between the Jones Library, Inc. and the City knowns as “Town of Amherst”?

April 25, 2023

Unique Issues Faced by Non-Profits in Bankruptcy

By Jody A. Bedenbaugh

Non-profits are just like for-profit companies in that they can be faced with significant financial challenges for which bankruptcy provides an opportunity for restructuring or liquidation for the benefit of their creditors and other stakeholders. Many times, particularly in the areas of healthcare and religious institutions, non-profit bankruptcies raise complex and novel insolvency issues. This blog post discusses four of the unique aspects of non-profit bankruptcies.

1. Non-profits are not subject to involuntary bankruptcy.

The United States Bankruptcy Code allows some parties to be put into bankruptcy by their creditors if certain conditions are met. This is referred to as an “involuntary” bankruptcy. Under Section 303(a) of the Bankruptcy Code, an involuntary bankruptcy case may not be brought against a corporation that is not a moneyed business or commercial corporation. Consequently, though non-profits may be indirectly forced into bankruptcy by an aggressive creditor or regulator through economic pressure, they cannot be placed into bankruptcy involuntarily by another party.

2. There is likely no “absolute priority” rule in non-profit Chapter 11 cases.

One of the requirements of the provisions governing plans of reorganization in Bankruptcy Code Section 1129(b) is that the plan must be “fair and equitable.” Section 1129(b)(2)(B) goes on to provide a statutorily defined requirement of the fair and equitable rule as it is applied to unsecured creditors, referred to as the “absolute priority rule,” which essentially requires senior classes (such as general unsecured debt) to be paid in full before the equity interest holders retain or receive any property under the plan if the senior classes do not approve the plan. Though there are various ways to satisfy the absolute priority rule while allowing current equity interests holders to retain their interests, the absolute priority rule is intended to maximize the payment to creditors from the disposition of the debtor’s property. In the case of a non-profit entity, however, courts generally hold that the absolute priority rule is not applicable because such entities do not have shareholders or equity interests. This gives non-profits additional flexibility in crafting plans of reorganization.

3. Non-Profit sales must comply with applicable non-bankruptcy law

As part of the 2005 amendments to Section 363(d)(1) of the Bankruptcy Code was added to state, “in the case of a debtor that is a corporation or trust that is not a moneyed business, commercial corporation, or trust, [a debtor or trustee may use or sell property under Section 363] only in accordance with non-bankruptcy law applicable to the transfer of property by a debtor that is such a corporation or trust. In addition, Section 541(f) of the Bankruptcy Code was added, which requires that property which is held by a 501(c)(3) debtor may be transferred to an entity that is not such a corporation only “if the transfer is in compliance with applicable non-bankruptcy law.” Finally, Section 1129(a)(16) was added to provide that a non-profit debtor may only transfer assets under a plan if non-bankruptcy law governing such transfers is observed. As a result of these provisions, any sale or transfer of assets by a non-profit pursuant to a bankruptcy case must still comply with applicable state law regarding such transactions by non-profit entities. Thus, for example, if a state attorney general must review and approve a sale of substantially all of a non-profit’s assets under state law like many healthcare businesses, the non-profit debtor must comply with those requirements in bankruptcy.

4. Non-profits may continue to consider their charitable mission while in bankruptcy

It is recognized that an insolvent company in or outside of bankruptcy should consider the interests of its creditors in its decision making. In the non-profit context, however, there may be tension between this duty to creditors and the debtor’s duty to further its charitable mission. Consider a situation faced by a non-profit hospital: it has a charitable mission of providing and preserving healthcare for the people in its service area, while the interests of creditors may be served by cutting services or selling assets to for-profit organizations. At least two courts have recognized that a non-profit’s duty to its charitable mission may be considered along with a debtor’s duties to its creditors. See In re United Healthcare Sys., Inc., 1997 BL 8656 (D.N.J. Mar. 27, 1997); In re HHH Choices Health Plan LLC, 554 B.R. 687 (Bankr. S.D.N.Y. 2016). Therefore, there is some support for the argument that the successful bid in the sale of a non-profit’s business should not be based only on the highest price and the bidder who is most likely to be able to fund the transaction — but may also include consideration of the buyer who is best able to preserve the charitable mission of the non-profit debtor.

Rob, So does this mean that the Jones Library can file for bankruptcy and the Town of Amherst would be responsible for the $9m the library currently owes the town for their share of the new library construction? Who is currently liable for this $9m debt..the town or the non-profit Jones?

It’s hard to imagine that the predictable mess that is being made of the libraries operating funds won’t have an effect on the hours of operation and level of service. Is there any way that services and hours of the Munson and North Amherst branches can be protected from this?

the classic case of group think is explained here (though in our case, 2/3 group think is sufficient): https://www.youtube.com/watch?v=USJ8OSIjhvk&t=16s

Good questions, KC and LC: the (city known as the) Town of Amherst issues the long-term bonds (and takes out the short-term loans) to fund the Jones Library project, so that appears to be where the debt obligation ultimately rests; there’s a memorandum of agreement between the Jones Library and the Town which outlines what’s expected by way of reimbursement, but whether that rises to the level of a formal debt obligation remains unclear.

I’ve asked the chair of the Finance Committee about this, and perhaps we’ll all get an answer (or clarification) directly from her, but the main thrust of the guidance I quoted above is that the law (item 1) protects non-profits like the Jones from being forced into bankruptcy to satisfy its debt obligations, and that (item 4) carrying out mission of the Jones — providing library services to Amherst — may take precedent over those debt obligations.

And practically speaking, unless private funding sources contribute a lot more to the Jones capital campaign, funds taken from the Jones endowment to satisfy any debt obligations to the Town would simply diminish what that same endowment should be contributing to the ongoing operation of the Jones Library itself.

So it would be great if a (very-deep-pocketed) private funding source were to step forward, and readers can likely think of at least one such source nearby….

… For example, a generous 1-to-1 match offer by such a deep-pocketed private institution of $1M per year over 3 years would go a long way to solving the problem.

At their FEB 20 meeting, the Jones trustees proposed using their endowment (valued at $9.24M at the time) to cover library operating expenses AND to reimburse the town for the library’s share of construction costs. They have proposed to take out $5M from the endowment to cover their fundraising shortfall. According to the cash flow referenced in the MOU with the town, they are currently over $6 million behind in payments, with another more than $2 million due by the end of the project. Any money not received by the town must be borrowed to cover construction expenses, and the town pays all interest on these loans. The Trustees also proposed increasing the annual draw from the endowment from 2.9% ($250,000/year) per year to 4.8% ($417,000) per year to cover the growing costs of operating expenses.

Is this sustainable? Or is it magical thinking?

The Library ought to be sharing its detailed fiscal projections with the Finance Committee and the public, lest the endowment dwindle rapidly, resulting in a demand for the town to fully cover the library’s operating budget.

To Arts comment .

It is magical thinking .The rule of thumb for withdrawals from your IRA would be 4 percent .

To increase the withdrawal rate to 4.8 and then to commit $5,000,000 to cover the short fall is not sustainable ,

They shouldn’t increase the withdrawal rate ,while simultaneously draining the capital . Unless ,they want to deplete the endowment .

There’s more than one private endowment in Amherst, and one is of mammoth proportions in comparison to that of the Jones Library.

Brother, can you spare a dime?

Important question:

What was the value of the Jones endowment at the close of business yesterday after the crash of AI-related companies and the huge war-related increases in the cost of energy over the winter?

I don’t see any hope for improvement in the next 12 months.

Why are we sleepwalking into the most obvious financial quagmire imaginable? The total cost is so beyond the realm of reasonable I have no idea how the project even got off the ground. There is no way the building they want to do actually costs this much. They’re not gonna be able to come up with the money. This is going to go badly in a really predictable manner.

WHY?? ….. people avoided telling the truth, the warnings of people who were concerned about the possible outcomes of this project were mostly ignored, and the so called “experts” in charge seem to lack good financial planning skills.

Look back at the comments made by those who tried to express their concerns about the dangers of entering into this renovation.